The increasing regulation designed to reduce the riskiness of banks after the global financial crisis has made more expensive and difficult for these institutions to lend. Banks have reacted reducing future lending activities to the private sector, creating a diminution of the capital available to fast growing mid-market businesses and consumers. Consequently, direct lending has emerged as a clear option to fulfill this financing gap, starting a disintermediation process that is driving a wide range of investment opportunities for private lenders.

The aforementioned disintermediation is also creating opportunities for borrowers. For businesses and consumers, they can get access to financing options that were previously only open to large corporations. For instance, small and medium firms have historically relied heavily on bank lending, since these companies´ borrowings do not justify issuing bonds in the public markets. As non-bank lenders – defined as financial firms that lend to businesses, but do not accept deposits – emerge, a recent survey revealed that some four-fifths (79%) of the respondents are now positively inclined towards these institutions, demonstrating a clear acceptance of the opportunity[i].

In addition to this, there has been a steadily increasing appetite for credit coming from business borrowers who lack sufficient access to traditional sources of consumer credit. Out of the sources of non-bank finance available, over half of companies (56%) have used credit funds, followed by private equity firms with a direct lending arm (49%), junior debt funds (40%) and asset backed lenders (39%)[ii].

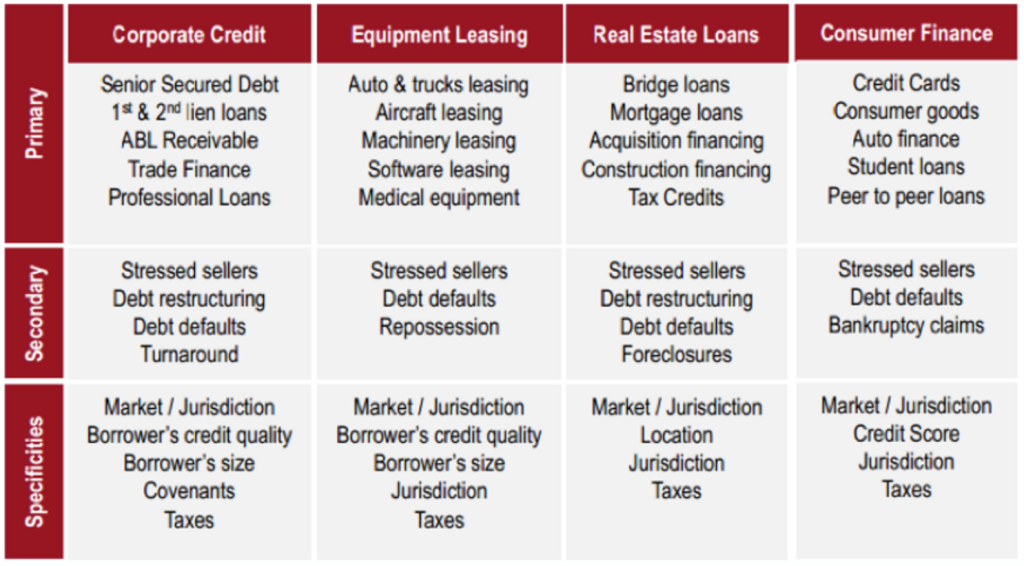

From an investor´s perspective, they have now access to investment opportunities that were previously limited to the extent of the banks. Many non-bank lenders have stepped in to fill this void, including alternative asset managers, hedge funds and private debt funds. Investors have identified four main segments within the private debt universe: corporate credit, equipment leasing, real estate and consumer finance. These strategies are summarized below, both in the primary and secondary markets.

The Private Debt Universe. Corporate Credits are private agreements between a corporation and a private lender and are generally backed by some type of assets. In the case of Equipment Leasing, the private lender often retains the right on the assets, while the borrower pays his liability directly to the lender. Opportunities for private lenders in Real Estate Financing include mortgages, bridges or more specific financing for construction and real estate acquisition. Consumer Finance includes credit cards, consumer goods financing and student loans. This segment has grown in recent years because of advantages in technology that makes peer-to-peer transaction easier.

Source: Crescendo and Mirabaud Asset Management

To access non-bank lending opportunities, asset managers need large teams of specialists to source and analyze each private lending opportunity. Alternatively, investors can also access this asset class via alternative lenders who typically build a diversified portfolio of loans across a range of different corporate sectors.

At this point fund manager selection is key. Successful alternative lenders to the middle market sector are able to negotiate specific loan terms that reflect the relative illiquidity of the loan, identify good companies in different geographies and sectors and structure robust loan documentation across different market cycles[iii].

Private debt is also becoming a relevant sub-asset class for institutional investors from a portfolio management perspective. The allocation to private credit markets helps complement a portfolio of traditional income investments (Bonds, REITs, etc.) with both a lower correlation and price volatility, since investments are not subject to mark-to-market fluctuation.

Incorporating direct lending to a portfolio will depend on the investor´s tolerance for adding illiquid assets[iv], although they may re-allocate some of the illiquid part of their portfolio to private debt[v]. More than two-thirds of the institutional investors are active in or are considering investing in private debt, although many institutional investors do not have a target allocation, committing capital from fixed income, private equity or general alternatives buckets[vi].

In addition to low correlation and reduced volatility, alternative lenders have a more active role in monitoring investments than high yield or investment grade investors. They have also greater information rights than investors in large deals and a stronger relationship with the issuers, being in a better negotiating position compared to investing in public bonds. These direct negotiations with management contribute to a better understanding of the credits and tighter covenants, resulting in an early control of the decisions in a downside scenario, preserving value and improve recovery rates[vii].

Lastly, there is a matter of access. Private debt not only allows lenders to provide loans to corporations, but also include other segment of the credit market not available to public credit investors such as consumer finance, equipment leasing or peer-to-peer lending.

To conclude, private debt as an emerging asset class offers attractive opportunities to investors looking to diversify their portfolio, with investments that provide a higher expected return with a lower correlation to traditional fixed income investments.

Private credit investors have access to a diverse set of opportunities in a market that has still room to grow. On the supply side, the disintermediation process continues to evolve, with banks still de-leveraging and reducing their loans to mid-market companies and consumers. On the demand side, despite the clear benefits non-bank lenders present, low levels of penetration within borrowers still persist, with only 21% of the mid-market corporates that have not yet used non-bank lenders would consider doing so in the future.

[i] Grand Thornton, Non-bank lending fuels growth opportunities for the mid-market – See more at: http://www.grant-thornton.co.uk/en/media-centre/news/2014/non-bank-lending-fuels-growth-opportunities-for-the-mid-market/#sthash.9QsBeZfd.dpuf

[ii] Grand Thornton, Non-bank lending fuels growth opportunities for the mid-market – See more at: http://www.grant-thornton.co.uk/en/media-centre/news/2014/non-bank-lending-fuels-growth-opportunities-for-the-mid-market/#sthash.9QsBeZfd.dpuf

[iii] Tom Sargeant, “Bypassing the middle man – opportunities in direct lending”

[iv] A good example of it replacing high yield bonds with direct lending, sacrificing liquidity but adding a competitive yield, a more senior position in the capital structure and a floating rate rather than a fixed one.

[v] Beyond Banks: The Emerging Opportunity in European Direct Lending – See more at: http://us.bnymellonam.com/core/library/documents/knowledge/market_commentary/sISSG_EuropeanDL.pdf

[vi] Preqin Special Report: Private Debt: The New Alternative? – See more at: https://www.preqin.com/docs/reports/Preqin_Special_Report_Private_Debt_Jul_14.pdf

[vii] Tom Sargeant, “Bypassing the middle man – opportunities in direct lending”

© 2024 ALTMENT

CAPITAL PARTNERS

© 2024 ALTMENT

CAPITAL PARTNERS

We use our own and third-party cookies for analytical and technical purposes; processing data necessary for the creation of profiles based on your browsing habits. You can get more information and configure your preferences from 'Cookie settings'.